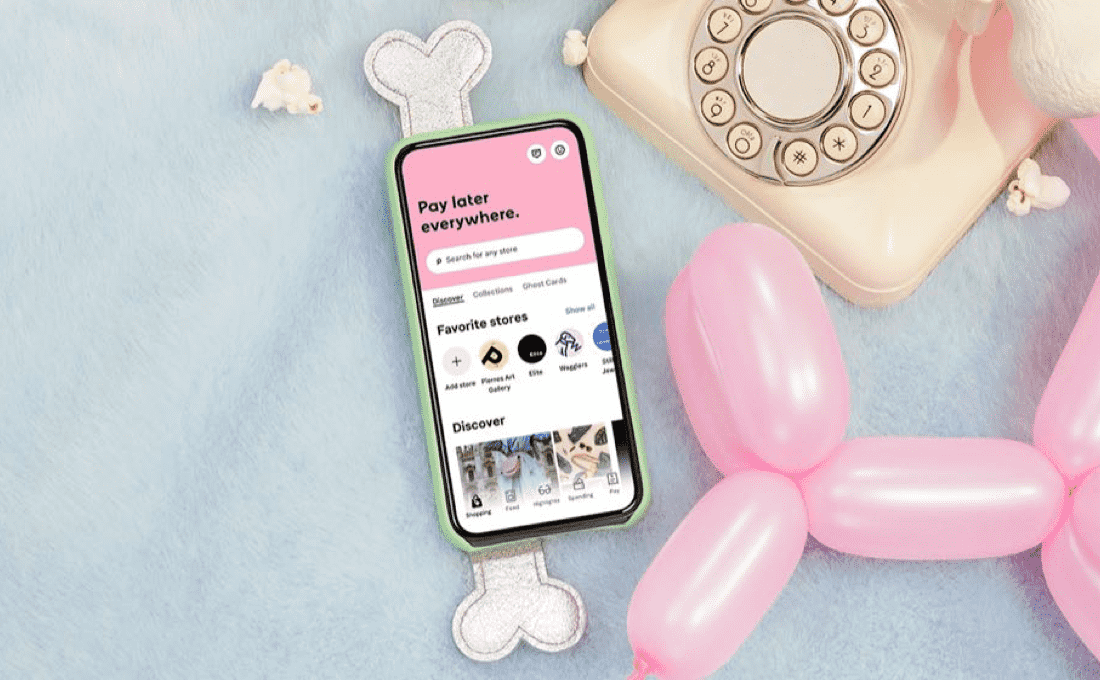

Klarna

Shop now, pay later with Klarna.

We’ve partnered with Klarna to give you a better shopping experience.

It’s smoooth and simple

Klarna helps you elevate your shopping game. When you choose Klarna at checkout, you’ll get the option to shop now and pay later for your purchase. It's shopping the way it should be. Effortless, safe and fun. That’s what we call smoooth (yes, so smoooth it needs 3 o’s).

Pay in 30 days

Make your purchase today and start enjoying what you’ve ordered right away. Pay up to 30 days after shipping and enjoy payment empowerment and peace of mind. No interest. No fees.

Financing

Apply for monthly financing during checkout. It’s a simple, 2-step application process with an instant decision. When approved, you can manage your payments and get payment reminders in the Klarna app.

Pay in 3 instalments

Split your purchase into three equal payments so you can spread the cost of your purchase over time. Enter the credit or debit card details of your choice and make automatic payments every 30 days. Your first instalment will be collected when your order is confirmed by the merchant and instalments 2 and 3 are scheduled 30 and 60 days later, respectively. No interest or fees.

How to shop with Klarna

Add item(s) to your cart and head to the checkout.

Select Klarna at the checkout to pay as you like for your purchase.

Manage your orders and payments in the Klarna app.

The best way to shop.

See all of your purchases in one place, pay any open balances, explore unique content and much more in the Klarna app. You can also log into your Klarna account at https://app.klarna.com/login. If you need any help, our Customer Service is there for you.

Safe and secure.

Klarna has strong anti-fraud controls in place to protect our customers and prevent fraudsters from making unauthorized purchases.

Frequently Asked Questions

Don’t see your question here? Visit our FAQ page to find out more about using Klarna. You can reach Klarna at https://www.klarna.com/uk/customer-service/ or by downloading the Klarna app.

What happens if I make a return?

If you return some or all of your order, Klarna will issue you with a new statement as soon as the online store processes your return. Follow the retailer's return instructions and make sure to keep the tracking number of your return. Log into your Klarna account and select “Report a return” so that your statement is paused. As soon as the retailer has registered your return, we will send an adjusted invoice.

There's something wrong with my order. Do I still need to pay for it?

You do not need to pay for goods that are received damage, broken or faulty. Follow the retailers dispute instructions and make sure to “Report a problem” in your Klarna account to pause your statement until you’ve resolved the dispute with the retailer. As soon as the retailer has registered your cancellation or your return, the refund will be processed within 5-7 business days.

I have not received my order. What happens to my statement?

You do not need to pay the statement until you have received your order. Contact the retailer for an update on the delivery. Make sure to log into your Klarna account and “Report a problem” to pause your statement until you’ve received your order.

My statement is incorrect. What should I do?

If your statement does not match your order details, please contact the retailer directly for a correction of your statement. Make sure to log into your Klarna account and “Report a problem” to pause your statement until the details have been corrected.

About Klarna

Founded in Stockholm, Sweden, Klarna is one of Europe's fastest-growing companies and a leading alternative payment provider. Kla

Klarna Terms & Conditions

This agreement for running-account credit (“Agreement”) is made between Klarna and you to finance purchases that you pay for with your account under the Agreement (“the/your Account” or “Klarna Credit”) from online suppliers who accept this payment method (“Suppliers”). This Agreement will be made and come into force if, after you have electronically signed this agreement form, we accept your application for credit and give you written confirmation that the Agreement has been made.

1. Your Credit Limit

We will determine your credit limit when we open your Account and give you notice of it. We will review your credit limit from time to time. We may increase your credit limit from time to time and will notify you of any change. If you do not want us to increase your limit without your request, you can tell us not to. We may also assess your eligibility for a credit limit increase when you take steps towards making a purchase with your Account that would take you over your current credit limit.

We may also reduce your credit limit but not so as to take it below the outstanding balance on the Account. We will notify you of a reduction in your credit limit before it takes effect.

2. Your use of the Account

We will provide you with credit on the terms set out below by allowing you to pay for online purchases from Suppliers (“Purchases”) with your Account. When you make a Purchase with your Account, we will pay the Supplier on your behalf and you will repay us in accordance with the terms of this Agreement.

You may use your Account to make Purchases provided that the balance of credit, interest, charges and fees outstanding are not taken over the credit limit and provided that you have kept up to date with your minimum monthly payments. The Account may only be used by you and you must inform us as soon as possible if you suspect any unauthorized use of it. We may suspend your right to credit under this Agreement in accordance with Section 8 below.

We may allow you to temporarily exceed your credit limit if you meet our credit assessment criteria at that time. There will be no charge for exceeding your limit.

3. Interest

For any Purchase made with the Account, “the Transaction Date” is the day when the goods are dispatched or, for a service, when the service is made available to you. Interest is charged, starting on the Transaction Date, on the balance outstanding on your Account for Purchases, with each Purchase being added to the balance on its Transaction Date. Interest is calculated on a daily basis and added to your Account each month on the date we produce your statement.

3.1 Standard Rate

The standard interest rate is 0.047 % per day, which results in an effective annual rate of 18.9 %. (“Standard Rate”). It is charged daily on the balance outstanding of all Purchases other than Special Purchases. The Standard Rate is also charged on fees (if any) on which interest has become payable.

3.2 Special Purchases

We may make special offers to you, for certain Purchases, which may include a reduced rate of interest or no interest for a particular period, a specific repayment schedule and other terms that affect the way you repay the credit for such Purchases (“Special Purchases”). Special Purchase offers are made at our discretion, are not available for all Purchases and cannot be changed by customer request.

3.2.1 Buy Now, Pay Later Purchases

If you take up a Buy Now, Pay Later offer, you will not be charged interest in respect of the Buy Now, Pay Later Purchase provided that you repay the entire Purchase by the end of a period which will be specified in the checkout before you make the Purchase (“the Buy Now Later Period”). The Buy Now, Pay Later Period may differ between Purchases. We may charge a fee for a Buy Now, Pay Later Purchase. Any fee will be specified in the checkout before you make the Purchase.

If a Buy Now, Pay Later Purchase has not been repaid in full by the end of the Buy Now, Pay Later Period, interest will be charged on the outstanding amount at the Standard Rate, starting with the day after the end of the Buy Now, Pay Later Period. A Buy Now, Pay Later Period will always end on a date when a monthly payment falls due.

3.2.2. Planned Payment Purchases

If you take up a Planned Payment offer for a Purchase, the credit for that Purchase (“Planned Payment Purchase”) must be repaid in full by the equal monthly payments which will be shown in the checkout before you make the Purchase. The payments will include interest, which will be charged at a fixed rate stated in the checkout, starting on the day after the Transaction Date.

You can stop paying the Planned Payment Purchase payment at any time and, instead, just pay the Minimum Payment but if you do stop paying the Planned Payment Purchase payment, the Purchase will no longer be a Planned Payment Purchase and the Standard Rate will be charged on the Purchase starting on the day after the first payment date when you do not pay a Planned Payment Purchase payment for that Purchase.

3.2.3 Reduced Interest Purchases

If you take up a Reduced Interest offer for a Purchase, a lower rate of interest than the Standard Rate will be charged on that Purchase (“Reduced Interest Purchase”) until the end of the Reduced Interest Period. The applicable rate of interest and Reduced Interest Period for a specific Purchase will be stated in the checkout before you make the Reduced Interest Purchase.

After the end of the Reduced Interest Period, the Purchase will no longer be a Reduced Interest Purchase and interest will be charged on any outstanding balance for that Purchase at the Standard Rate.

If you fail to make a Minimum Payment by its due date, any Reduced Interest Purchases will cease to be treated as Reduced Interest Purchases and interest will be charged on the outstanding balance of any such Purchases at the Standard Rate, starting on the payment date when that Minimum Payment fell due.

3.3 Minimum Charge

There will be a minimum charge of £1 per month, so that if the interest incurred on the daily balances outstanding for Purchases during the period to which the statement relates (“Purchase Interest”) is less than £1 for any month, taking into account any interest charged at the Standard Rate as well as any interest charged at a special rate for a Special Purchase, there will be a charge equal to the amount required to take the total amount of interest charged for that month up to £1 (“Minimum Charge”). The Minimum Charge will not apply to zero balances.

4. Your Monthly Repayments

Whenever any part of the balance outstanding on your account includes a Planned Payment Purchase or a Reduced Interest Purchase, your monthly statement will show two alternative payments: the Minimum Payment and the Interest-saver Payment. You can always pay more than the Minimum Payment or the Interest-saver Payment if you want to.

You must pay at least the Minimum Payment towards repayment of the full balance on your Account each month. The amount of the

Minimum Payment will be equal to:

The higher of

(i) The sum of

a) 1% of the total balance of all Purchases on your Account + Purchase Interest or any Minimum Charge for the period to which the statement relates; and

b) any Late Payment Fees, Paper Statement Fees, Debt Collection Fees and interest on such fees incurred in that period;

(ii) Or; £5 up to the total outstanding balance on your account.

Alternatively, you can pay the “Interest-saver Payment”. This will allow you to avoid paying interest on any Buy Now, Pay Later Purchases for which the Buy Now, Pay Later Period is ending, and to preserve preferential interest rates for the balances of any other Special Purchases you may have on your Account. The amount of the Interest-saver Payment will be equal to:

a) The full balance of any Buy Now, Pay Later Purchases for which the Buy Now, Pay Later Period is ending b) The planned payment(s) for any Planned Payment Purchase(s)

c) The higher of

(i) The sum of;

a. 1% of the total balance outstanding on your Account for Purchases other than any Buy Now, Pay Later

Purchases and Planned Payment Purchases + Purchase Interest other than Purchase Interest for any Planned

Payment Purchase(s) or any Minimum Charge for the period to which the statement relates; and

b. any Late Payment Fees and Paper Statement Fees, Debt Collection Fees or interest on such fees incurred in that period;

(ii) OR; £5

The Interest-saver Payment or the Minimum Payment must reach your Account by the due date on the monthly statement we will send you. If you fail to make the Minimum Payment, we will charge a late payment fee of up to £ 12.

5. Monthly Statements

We will send you a statement each month, unless there has been no activity on your Account that month. There may be no activity on your Account when, for example, you only have a Buy Now, Pay Later Purchase on your Account which you purchased in an earlier month and for which the Buy Now, Pay Later Period is not coming to an end.

Your monthly statement will show the balance at the start of the period to which it relates, the date and amount of any balance changes (Purchases made, interest and fees incurred, and payments made into the Account since the period covered by the last statement) and the outstanding balance on your Account. It will also show the Minimum Payment required and, if applicable, the Interest-saver Payment. The monthly statement will also state if you have failed to make the Minimum Payment for any previous billing periods.

6. How we Allocate your Payments

We will apply any payment into the Account as follows:

1) First, in paying any overdue Minimum Payments from earlier billing periods;

2) Then in meeting any Minimum Payment then due;

3) Then in paying the difference between any Minimum Payment then due and any Interest-saver Payment then due, including any Purchase Interest or any Minimum Charge; and

4) Then in making an early repayment.

We will allocate so much of any payment into the Account as does not exceed the amount required to meet any Minimum Payment then due:

1) First in paying any Minimum Charge, Late Payment Fee, any Paper Statement Fee, any Debt Collection Fee and any interest on any Fees;

2) Then in or towards paying any Planned Payment Purchase payments then due, so that the payment is allocated towards Planned Payment Purchases with higher interest rates before Planned Payment Purchases with lower interest rates; and

3) Then in or towards repaying the balance outstanding in respect of all Purchases other than Buy Now, Pay Later

Purchases for which the Buy Now, Pay Later Period has not yet come to an end.

Then we will allocate the amount by which any payment into the Account exceeds any Minimum Payment then due, up to the amount of any Interest Saver Payment then due:

4) First, in repayment of the remaining outstanding balance of any Buy Now, Pay Later Purchase for which the Buy Now, Pay Later Period is ending on the date of the payment or between the date of the payment and the date of the next monthly statement;

5) Then in repayment of the remaining balance of any Planned Payment Purchase payments then due so that Planned

Payment Purchases with higher interest rates are paid off before Planned Payment Purchases with lower interest rates.

Lastly we will apply the amount by which any payment into the Account exceeds the amount of any Interest-saver Payment then due:

6) First in repaying the balance outstanding in respect of all Purchases other than Special Purchases;

7) Then in repaying the balances outstanding for interest-bearing Special Purchases, so that balances for Purchases with higher rates of interest are paid off before balances for Purchases with lower rates of interest; and

8) Then in repayment of any Buy Now, Pay Later Purchases for which the Buy Now, Pay Later Periods have not come to an end.

Subject to the order set out above, earlier Purchases will be repaid before later Purchases and Purchases which have been shown on a monthly statement will be paid before those which have not yet been shown on a monthly statement.

7. Early Repayment

You have the right to repay all or part of the credit early at any time at no extra cost. We will let you know the balance outstanding upon request.

8. Our right to refuse transactions and suspend your Account

We may refuse to authorize a purchase or suspend your right to make purchases with your Account for any of the following reasons a) Your purchasing behaviour seems unusual compared with the way you normally use your Account;

b) We suspect that unauthorized or fraudulent use is being made of your Account under the Agreement;

c) There is any legal or technical restriction which prevents us from lawfully providing you with credit at the time when you attempt to make a purchase using your Account;

d) You fail to make any payment which falls due to us under this Agreement or under any other agreement that you may have with us when that payment falls due;

e) We believe that there is a significantly increased risk that you may not be able to fulfil your duty to repay the credit in accordance with this Agreement (this includes situations such as you going bankrupt or having similar proceedings

taken against you);

f) We reasonably believe the transaction would damage our reputation;

g) You have not used your Account to make new purchases for at least two months;

h) There is any other objectively justifiable reason.

If we decide to refuse a transaction or suspend your right to use the Account, we will give you notice by email as soon as practicable.

9. Our right of set-off

If we owe you any money we will be entitled to set-off the sum we owe you against any debt you owe us under this Agreement.

10. Fees

We charge the following fees:

- Up to £12 if you do not make your Minimum Payment on time (“Late Payment Fee”);

- £1.49 for each Paper Statement Fee;

- The reasonable cost of sending you a letter about your outstanding debt when you are in arrears (“Debt Collection

Fee”).

Any fee which becomes payable under this Agreement will be added to the balance on the payment date following the statement for the month in which the fee became payable. We will start charging interest at the Standard Rate on Late Payment Fees and Debt Collection Fees on the 29th day after we have given you notice that the fee has become payable.

11. Changes to this Agreement

We may change the interest rates and/or fees or charges payable under your Agreement to take account of changes in the cost of providing credit to you or to reflect the cost of any system or product development. We may also change and add to the other terms of this Agreement to respond to changes in legal or other regulatory requirements or to reflect new industry guidance or codes.

Our power, under this term of this Agreement, to vary any fees or charges includes the power to remove or add fees or charges for the reasons given above without first obtaining your consent. We will give you written notice of any such change and the change will come into force 60 days after the notice has been sent. You may end this Agreement in accordance with clause 15 if you do not want the change to apply to your Agreement.

12. APR and Total Charge for Credit

If you were to use your Account to make a Purchase of £1,200 on the date when this Agreement is made, to repay that amount by making 12 equal monthly payments, together with the interest which is payable on each payment date in accordance with clauses 3 and 4 of this Agreement, the total amount payable would be £1,326.37 and the APR would be 18.9 %. This assumes that the Standard Rate of interest would apply and that no change would be made to the Standard Rate during that period.

13. Right of withdrawal

You have a right under the Consumer Credit Act 1974 to withdraw from this Agreement without having to give any reason. To exercise your right of withdrawal you must give notice of your intention to withdraw from the Agreement before the end of 14 days beginning with the day after the day on which you receive a copy of the Agreement signed by us, unless you have received an earlier copy, in which event the 14 day period will begin on the day after you the day you receive our written confirmation that the Agreement has been made on the same terms as set out in the earlier copy. You must give notice of withdrawal by telephone or in writing to our business address or by email (please see our contact details at the beginning of this Agreement).

You must repay the amount of credit provided under this Agreement, together with interest, without delay and no later than 30 calendar days after giving notice of withdrawal. We will inform you of the amount of interest payable on request and without delay. You must make payment to Klarna by calling +44(0)2030050833 and paying by credit or debit card or by bank transfer in accordance with the instructions given to you.

Please note that withdrawing from your Agreement with us will not terminate your purchase agreement(s) with the Supplier(s). Your rights in relation to your agreements with Suppliers are governed by those agreements and the legislation relating to them.

14. Consequences of default and missed payments

If at any time, two or more Minimum Payments are overdue, we may serve a default notice on you, requiring that you bring the Minimum Payments up to date. If you then fail to do so, we may, by giving you written notice, terminate the Agreement and/or require that you make immediate repayment of the outstanding balance of credit, interest and any fees on the Account.

After termination under this clause 15, we may employ a debt collection agency to recover the outstanding debt and you will have to pay reasonable costs incurred by the debt collection agency for this purpose.

Missing payments can have serious consequences for you. Your credit rating may be affected which will make it more difficult or more expensive for you to obtain credit in the future. Legal action may be taken against you to recover the debt, an application may be made to have you declared bankrupt, and it is possible that a charging order and order for sale of your property may be obtained as a means of enforcing any judgment.

15. Termination of the agreement

This Agreement has no fixed duration and will continue until either we or you terminate the Agreement.

You can bring this Agreement to an end at any time with immediate effect, and without having to give any reason, by giving us not less than seven days’ oral or written notice.

We can bring the agreement to an end by giving you two months’ written notice.

If you become bankrupt or are unable to pay your debts or if an interim order in bankruptcy is presented or made, or you become apparently insolvent or have a proposal for a voluntary arrangement made in relation to you, we may, by giving you written notice, bring this Agreement to an end immediately.

If we or you end this agreement you must continue to make your Minimum Payments until you have repaid all amounts you owe us.

16. Consent to electronic communication, correspondence and change of details

When you give your consent to us sending electronic communications to the e-mail address or telephone number you have provided, you agree that we may send monthly statements, notices and other communications under or in relation to the Agreement (other than communications that are required by law to be sent in paper form) via email to this e-mail address or via text message to this mobile phone number.

You must promptly inform us of any changes to your name, address, email or telephone number. You must provide any evidence of such changes that we may reasonably require.

All communication between you and us in relation to this Agreement shall be in English.

17. Assignment

You may not transfer or assign any rights or obligations you have under this Agreement without our prior written consent. We have the right to transfer or assign this Agreement or any right or obligation under this Agreement at any time without your consent, provided that such transfer does not alter your rights and obligations under this Agreement to your detriment.

18. Our liability to you

You may have the right to sue a Merchant or us or both if you have received unsatisfactory goods or services paid for under the Agreement costing more than £100 and not more than £30,000. Except for that right in respect of misrepresentation or breach of contract relating to your agreement with the Merchant, we shall not be liable to you for any loss of profit, goodwill, business, revenue, data, anticipated savings or other loss or damage which does not arise directly from a breach of this Agreement by us. Nothing in these terms and conditions excludes or limits liability for death or personal injury caused by negligence, fraudulent misrepresentation, or your statutory rights as a consumer, or any other liability which may not otherwise be limited or excluded under any applicable law.

19. Our use of your personal data

You acknowledge and agree that we may collect and otherwise process your personal data as described in this paragraph 20 when you use Klarna’s services, including: your first and last name, title, address(es), date of birth, gender, email address, IP address, browser and device information, telephone number, and information about your payment and order history at the e-store(s) used, and at Klarna, such as the number of items, item number, invoice amount, delivery method, track and trace number, and tax percentages).

We will process such personal data for identification and credit assessment, risk management, development of Klarna’s services, relationship management, marketing (as described in our Privacy Statement at www.klarna.com/uk), internal statistical and analytical purposes, and for investigation of fraud or other misuse of service. Klarna may also use information available on the internet for the purpose of identification when we deem further investigation to be necessary, as well as for investigation of fraud and other misuse of services.

For information about what data we transfer to credit reference agencies, and for what purposes, please refer to Section 21 below and to the Privacy Statement on www.klarna.com/uk. Our privacy statement contains more detailed information on how we handle personal data, such as collection (including information you give us and information we collect about you), how we use personal data, details of how and why we disclose and transfer your personal data and information about your statutory rights.

20. Information to and from credit reference agencies

When you apply for an Account, we make a full credit search with credit reference agencies who will supply us with credit information. The agencies will record details of the search, which can be seen on your credit file, whether or not credit is granted. This record will also be visible to third parties and may affect other organizations’ future decisions on whether or not to provide you with credit.

We will report information to credit reference agencies about the payments you make, and about any payments that you fail to make on time.

If we do not grant your credit application, you will receive a failure notice from us. If your decision not to grant your application for credit is based on information supplied by a credit reference agency, we will provide you with details of the agency via email.

21. Supervisory authority

The supervisory authority of this Agreement is the Financial Conduct Authority, 25 The North Colonnade, Canary Wharf, London E14 5HS.

Klarna is a bank authorized by Finansinspektionen (the Swedish Financial Supervisory Authority), (www.fi.se, Box 7821, 103 97 Stockholm) to provide financial services. Klarna is registered with the Swedish companies register under number 0556737-0431.

22. Complaints

If for some reason you are dissatisfied with our services, we will do our best to resolve the matter as soon as possible. You can reach us via email, letter or phone at the addresses/numbers provided in the beginning of this Credit Agreement. You can also reach our customer service agents via our online chat service (https://www.klarna.com/uk/customerservice) at business hours.

If we do not resolve your complaint to your satisfaction, you have the right to refer your complaint to the Financial Ombudsman Service by calling 08000234567 or using the online form available at https://www.financial-ombudsman.org.uk/contact/index.html or writing at Exchange Tower, Harbour Exchange, London, E14 9SR.

24. Governing law

This Agreement is governed by the laws of England and is subject to the non-exclusive jurisdiction of courts of England and Wales. If you are a resident of Northern Ireland you may also bring proceedings in Northern Ireland, and if you are a resident of Scotland, you may also bring proceedings in Scotland.

25. General

If at any time we allow any time for remedy of a breach, or if otherwise we do not insist on our strict rights under the Agreement, this will not prevent us from insisting on our strict rights on another occasion. If we agree to a variation on one occasion, it does not mean that we must agree to it on another occasion.

Any provision of this agreement which expressly or by implication is intended to come into or continue in force on or after termination of this agreement shall remain in full force and effect.

This Agreement does not affect or exclude any term implied by law unless it expressly says so.

If any term in this Agreement shall not be enforceable, it will not affect the enforceability of all other terms.

If your application for running-account credit from Klarna is approved, you will receive confirmation from Klarna and you will be able to finalise your purchase with your account. You will receive a copy of your credit agreement to your home address and an email with further information.

There is a requirement under UK law to withhold tax due on the payments but you will not need to do this or take any action based on the agreement we have with the UK tax office. You may if you wish, contact the tax office for further information and the details are: